Mortgage brokers and lenders have argued that the tightening of mortgage regulations in January 2018 adversely impacted the growth of mortgage lending in Canada.

A report released Tuesday by the Canada Mortgage and Housing Corporation confirmed this assertion, finding that 2018 saw the slowest growth rate of outstanding mortgages in a quarter-century.

Interestingly, the intervention-driven slowdown in the mortgage growth rate in 2018 was more severe than the housing market slowdown sparked by the Great Recession in 2008.

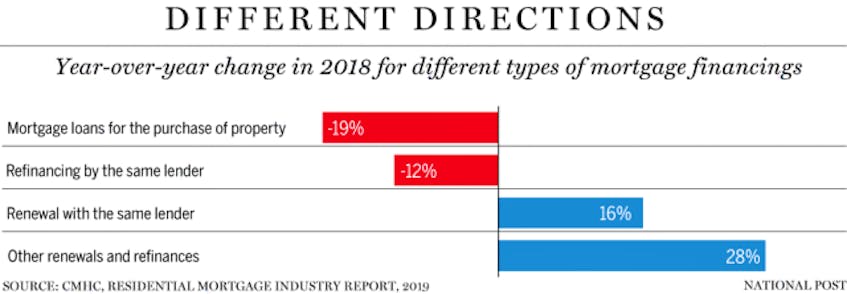

The CMHC’s inaugural Residential Mortgage Industry Report exposes the extent of the impact of regulatory changes, especially the tightening of the underwriting criteria, which affected the number of housing transactions (down by 11 per cent in 2018) and housing prices (down by four per cent). The cumulative impact of the changes resulted in a decline of 19 per cent in the demand for mortgages for the purchase of property.

The report also points to distortions introduced by the revised stress test implemented in January 2018, which required borrowers to qualify for a higher rate than the contracted mortgage rate.

Consider, for instance, that while refinancings with the same lender were down by 12 per cent in 2018, renewals with the same lender were up by 16 per cent.

The report noted that the renewals were “not specifically subject to the new stress test and are more likely to meet current lender criteria.”

The overall impact of these regulations meant a constrained choice set for borrowers who could not shop around at renewal and were constrained to negotiate with the same lender. This implies that the homeowners were more likely to stick to the same lender to avoid being subject to the stress test irrespective of their credit history or credit worthiness.

Another large impact of the regulatory changes is the 16-percentage-point decline in the share of insured mortgages, which fell from 57 per cent in the first quarter of 2015 to 41 per cent in 2019. The report suggested that the 2016 stress test for high-ratio mortgages was behind the shift to uninsured mortgages.

The CMHC report describes the four primary types of mortgage providers and their operating characteristics. In 2018, the chartered banks held the largest market share of mortgages accounting for no less than 75 per cent of the residential mortgage market share. The interest rates charged by the banks ranged from 3.3 to 5.4 per cent.

Credit unions and caisses populaires accounted for 14 per cent of the residential mortgage market share. The report did not disclose the interest rates charged by credit unions. Mortgage finance companies (MFCs), often not federally regulated, held a six per cent market share. Lastly, Mortgage Investment Corporations (MICs) and private lenders were estimated to have a market share of just one per cent.

Compared to the banks, MICs charged much higher interest rates that ranged between 7 and 15 per cent. At the same time, the mortgage delinquency rate for the MIC borrowers at 1.93 per cent was higher than that for those who borrowed from the banks or MFCs.

The much higher default rate for those borrowing from private lenders and MICs suggest that high-risk borrowers were pushed to lenders who offer high-price mortgage solutions, as is evidenced by the significantly higher interest rates, to account for the weak creditworthiness of their clients. At the same time, the excessively high cost of borrowing could also trigger higher than expected default rates.

The average loan size was the largest for the banks at $220,650 and the lowest for credit unions at $150,995. Private lenders and MICs issued loans with an average amount of $194,760.

The CMHC report explicitly demonstrates that regulatory changes could have a large impact on housing markets. At times, the regulation-driven impacts might be larger in magnitude than the ones resulting from an economic recession.

Changes in regulations could be successful in achieving the intended goals, such as imposing market discipline by limiting high-risk lending. A slowdown in housing sales and price appreciation could also be part of the intended outcomes, yet their larger impact on the overall economy might help stimulate the very undesirable market conditions the regulators intended to safeguard against.

Murtaza Haider is a professor of Real Estate Management at Ryerson University. Stephen Moranis is a real estate industry veteran. They can be reached at www.hmbulletin.com .

Copyright Postmedia Network Inc., 2019